Business for Sale Owner Financing

What is Owner Financing in Business Sales?

Owner financing, otherwise known as seller financing, is an ingenious and practical means of selling a business. In this case, the business owner steps into the shoes of a lender and works with the buyer to set a series of payments over time instead of demanding full payment up-front. Business for Sale Owner Financing

The process eliminates third-party financing involvement, unlike typical sales where banks or financial institutions provide lending options. This makes it highly conducive for someone who may have financial issues. A seller benefits from the sale as it provides a wider pool of buyers, and it can also hasten the sale since there are no lengthy check-clearing procedures.

Because owner financing provides a win-win relationship between buyers and sellers, it becomes comparatively popular in a competitive market of today.

How Does Owner Financing Work?

This involves an agreement based on a repayment schedule from the buyer, as set forth by the seller. It includes these typical steps:

Negotiating the Purchase Price: The total cost of the business is agreed upon by both parties.

Down Payment: The buyer makes a payment up-front as a first deposit, usually 10-30% of the purchase price, as an indication of the buyer’s good faith.

Promissory Note: A binding legal document is signed, showing the payment plan, interest rate, and repercussions if the buyer does not comply.

Installment Payment: The buyer regularly pays (monthly, quarterly, or annually) to the seller until the debt is paid off. Business for Sale Owner Financing

Benefits of Buying a Business with Owner Financing

Owner financing is advantageous in many ways for buyers. These include:

Lower Barriers to Entry: Even a less-than-perfect lender can buy a business with fewer hurdles than it would have faced in qualifying for a traditional loan. Business for Sale Owner Financing

Flexible payments: The payment schedule, the rate of interest, and the amounts payable can be arranged for every kind of buyer by the seller themselves in accord with their financial circumstances.

Lower Down Payments: Since financing allows for a lesser down payment, it leaves the buyer more cash for necessary reinvestments into the business and marketing efforts.

And for the sellers, the benefits are just as powerful:

Fast Sale Process: With owner financing as an option, the pool of potential buyers widens tremendously.

Second Income: The sellers can collect interest on the loaned amount, which may provide a continued stream of income after the sale.

Increased Negotiating Power: By offering financing, sellers gain the upper hand in negotiating for a higher selling price.

Common Types of Businesses Sold with Owner Financing

Owner financing is flexible and can be applied to almost any industry. The types of businesses commonly sold in owner financing include:

Retail businesses: such as clothing stores, gift stores, and specialty shops

Hospitality businesses: such as cafes, restaurants, and bed-and-breakfasts

Service businesses: such as salons, auto repair shops, and cleaning services

Small-Scale Manufacturing: small-scale production facilities to serve niche markets.

These businesses attract buyers because they are small enough to be manageable, offer a predictable earnings stream, and have a lower purchase price than larger businesses.

Key Considerations for Buyers and Sellers

Core Points should be Considered by Buyers and Sellers

For buyers:

Research: Ascertain the company’s standing in terms of financial history, operational records, and its market reputation.

Plan to Win Use the business plan envisaging the post-acquisition management and growth of the business.

Professional Advice: Let the lawyers and financial advisors sift through the minute details of the deal for you, thereby ensuring that all your interests have been duly taken into consideration.

For sellers,

Check Buyer’s Credentials: Verify his financial status, creditworthiness, and capacity to carry on business.

Secure Your Note: Your promissory note must state the terms of payment, at what rate of interest, and the event of any default by the buyer.

Discuss the tax impacts: Speak to a tax consultant regarding income on financing and how best this income fits in with the overall profit picture for refrigerator installations.

Effective communication is needed from both sides, with both having to agree on an appropriate contractual guarantee from lawyers, thus protecting their respective interests.

Challenges and Risks of Owner Financing

It may seem that owner financing is rather appealing, however, it is also risky.

For the buyer:

Payment Obligations: Default in payments can create legal issues and losses.

Interest Costs: The business price might finally add up to become considerable due to compounding interest.

For the seller:

Risk of Default: This means that the buyer may fail to make payments.

Extended Payment Period: The seller has to wait long until receiving the entire amount.

Careful planning and legal safety measures should ensure that risks to both remain minimized.

How to Find Businesses for Sale with Owner Financing

Some of the different paths that may lead you to the businesses offering owner financing include:

Online Marketplaces: Websites such as BizBuySell and BusinessBroker.net allow you to filter lists by financing possibilities.

Local Business Networks: Attend local gatherings of business enthusiasts and network with other insiders about how to find owner finance opportunities.

Business Brokers: Accomplished brokers arrange buyers with possible sellers who could accommodate negotiating the several conditions of financing arrangements.

You will get to see some matching opportunities regarding your financial goals and business interest while exploring these resources.

Is Owner Financing the Right Option for You?

Owner financing can offer an extremely good opportunity for buyers looking to acquire a business with little down and for sellers who need quick closure. Still, the arrangement would need serious consideration and planning to be successful.

Take time to evaluate the merits, challenges, and long-term consequences if you want to consider this option. Both buyers and sellers should seek professional input to navigate with enough certainty and feel confident in settling for a win-win arrangement.

Why Owner Financing is Gaining Popularity in Business Sales

There are a number of reasons why owner-financing is a very appealing option right now in the business sales market: It accelerates the closing of deals and widens the pool of buyers which includes those who may not qualify for traditional bank loans. This strategy is even more helpful in markets where the competition may compel buyers to seek flexible payment alternatives to reduce their cash outlay.

Less obstacles for buyers because of owner financing are an added plus. Without the hassles of waiting for a bank to approve the buyer, the chances for closing the deal arise sooner. Finally, that financing symbolizes trust on the part of the seller in the future success of the buyer. Also, in several cases, owner financing enables a higher sale price, as buyers may indeed pay more for favorable terms.

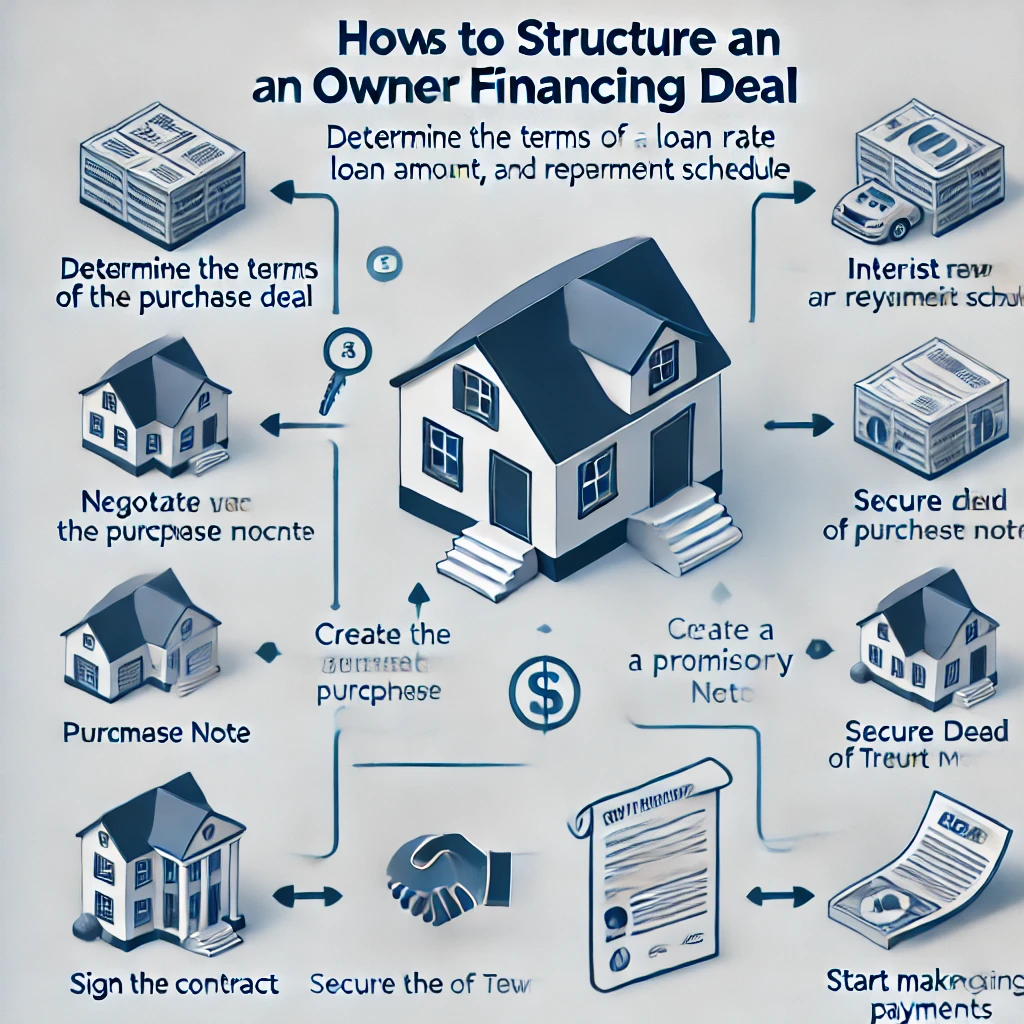

Steps to Structure an Owner Financing Deal

Creating a successful owner financing agreement requires careful planning and clear communication. Here are the critical steps to structure such a deal:

- Evaluate the Buyer’s Financial Background: Conduct a thorough review of the buyer’s credit history, financial stability, and ability to manage the business successfully.

- Negotiate the Down Payment: Agree on an initial payment that demonstrates the buyer’s commitment while reducing the seller’s risk.

- Set Clear Repayment Terms: Outline the loan’s duration, monthly payment amounts, and interest rates. Ensure that these terms are realistic and mutually acceptable.

- Draft a Promissory Note: This document serves as a legal agreement that includes repayment details, penalties for missed payments, and any contingencies.

- Secure Collateral: The seller should secure collateral, such as business assets, to protect their interests in case of default.

- Involve Professionals: Work with attorneys and accountants to ensure the agreement complies with legal and tax requirements.

By following these steps, both parties can establish a strong foundation for a smooth transaction.

Legal and Financial Documents Needed for Owner Financing

Proper documentation is essential to safeguard the interests of both buyers and sellers in owner-financed deals. The most important documents include:

- Promissory Note: Details the terms of the loan, including payment schedule, interest rates, and penalties for default.

- Security Agreement: Specifies which business assets are being used as collateral for the loan.

- Purchase Agreement: Outlines the complete terms of the sale, including the purchase price and responsibilities of each party.

- UCC-1 Financing Statement: A document filed with the relevant government agency to publicly record the seller’s lien on the business assets.

- Personal Guarantee: Provides an additional layer of security, ensuring the buyer’s personal assets can be claimed in case of default.

These documents not only ensure transparency but also provide legal recourse in case of disputes or non-payment.

Advantages and Disadvantages of Owner Financing

Owner financing comes with its own set of advantages and disadvantages.

Seller Benefits:

Speedy closing as opposed to waiting for bank financing.

Possibility of acquiring more income through interest payments.

Greater chance of selling business at a higher price, due to flexible terms.

Buyer Benefits:

Reduces difficulty in applying for finance.

Possibility to negotiate terms that will suit one’s ability to repay.

Seller Drawbacks:

Risky if the buyer defaults: this could lead to subsequent litigation.

Full payment may take a while, affecting the seller’s future plans regarding fund distribution.

Buyer Drawbacks:

Higher interest rates than a traditional loan.

Restrictions on exploitable business operations until full repayment.

How to Negotiate Terms for Owner Financing

Negotiation sets forth a blueprint for every owner-financed deal and is important for a successful agreement. Things to bargain on include:

Down Payment: The buyer and seller should agree on a large down payment to minimize risks for the seller and have it affordable for the buyer.

Interest Rate: The best interest rate will be competitive with but will not be unreasonable to the point where it becomes counterproductive to the transaction.

Repayment Terms: Payments should be scheduled as per the buyer’s cash flow, with the seller receiving regular income.

Loan Term: Specify the timeline for loan repayment, taking into account the seller’s business goals and the buyer’s ability to pay.

Default Clauses: The penalties for missing payments must be clearly defined, to avoid misunderstandings.

Common Mistakes to Avoid in Owner Financing Deals

Owner financing deals can go awry if handled improperly. Common pitfalls that occur include the following:

Poor Buyer Screening: Not screening the buyer’s qualifications can lead to sure loan defaults along the way.

Falling to Draft Legal Contracts: Skipping proper contracts could lead to conflicts or even financial loss.

Neglecting the Tax Aspects: Installments labored from the proceeds of sale would affect the seller’s tax obligations.

Unreasonable Payment Terms: Some terms may be either too harsh or too lenient for either party.

How to Market a Business for Sale with Owner Financing

To attract the right buyers, sellers must market their owner-financed business strategically. Tips include:

- Highlight Financing Options: Mention owner financing prominently in advertisements to attract interested buyers.

- Use Online Platforms: Websites like BizBuySell and local business listing sites are great places to advertise.

- Leverage Social Media: Share posts on platforms like LinkedIn and Facebook to reach a wider audience.

- Work with a Broker: Business brokers with experience in owner-financed sales can help market effectively.

This approach increases visibility and ensures you reach buyers actively seeking flexible financing options.

Tax Implications of Owner Financing for Sellers

The seller should see the tax impacts of owner financing. Evils include:

Installment Sales: Taxes would be paid over the course of the payment period, deferring immediate liabilities.

Interest Income: Seller earns interest which must be declared as taxable income.

But while doing so, sellers confront challenges like capital gain tax, and depreciation recapture would need to be countered. A consult with a tax professional yields compliance and strategic ways to maximize benefits.

Success Stories of Owner-Financed Business Sales

Real-life examples of successful owner-financed sales can be very informative. Consider these examples:

A small restaurant owner sold their business to a trusted manager with his owner financing such that a smooth transition takes place. Business for Sale Owner Financing

The founder more or less relied on owner financing to bring in a buyer for a tech startup, which allowed that buyer to later expand the business greatly.

Conclusion

Owner-financing presents one of the most flexible and quicker ways of buying or selling a business. Owner-financing enables a buyer to circumvent traditional financing problems. It provides less hassle for the sellers than dealing with a lengthy bank approval process.

But there are many risks in owner financing when it comes to buyer defaults or slow payments. Performing due diligence on the buyer, clear instructions, and working with a professional all go a long way toward ensuring a successful deal. Business for Sale Owner Financing

Since it is becoming increasingly popular, owner financing is one of those considered when looking for an easier, manageable option of business ownership. Finding a balance of pros and cons and delineating terms will help secure transaction goals in ways that are most efficient for both parties.